Permission Granted:

How to Finally Enjoy the Wealth You Built

Escape The Clock Insights

I’m exceptional with money. For most of my life that felt like the whole answer, and it turned out to be only half of one.

Our dishwasher broke when I was 10 years old. My mother was the only one “supposed” to do the dishes, but I saw how that drained her. I felt so bad for her and asked if I could help. She told me that what she really needed was a new dishwasher, but we couldn’t afford the $150. So, I got a paper route. I’d start work at 4 a.m., bagging the papers in the dark, so that I could rush the route and get every one on a porch by six. Most mornings I’d just make the bus stop by 7 a.m. But it was worth it. After three hard months, I had enough money to buy her that dishwasher and enough left over to buy my brothers each a toy. Everyone was so proud of me, and I’ll never forget the impact it made.

Once the hustle gets you, it’s hard to stop. By fourteen I got a “real” job bagging groceries at a Kroger in Columbus, Ohio, where the state capped me at ten hours a week and I spent every dollar of it feeding myself at school. Then there was a summer at Malibu Grand Prix to save for a car, a stretch at Service Merchandise to scrape together money for college, and a job working the phones for a truck dispatching company. Even a stint at Blockbuster Video, to cover the gap once I’d maxed out what I was allowed to borrow at The Ohio State University.

And that was just the beginning. As a junior in college I talked my way into a programming job at an HVAC company called LCSystems by swearing I could build anything they needed. I couldn’t, not yet at least, but I figured it out well enough, and I was still there the day I graduated. The job market in Columbus Ohio was so bad in 2004 that I got 15 seconds of fame on the local news for being one of the few in my graduating class with a job!

From there the treadmill only accelerated. I climbed, never staying anywhere longer than two years, company to company, until I was at Microsoft outpacing people who’d been there two decades longer than me. Then Google called, and I left to lead some of the largest programs in its cloud business, all of it while raising a family and inching toward the day I could finally stop.

Here’s what a lifetime of that builds: a master of the dollar. By the time I retired at 43, I could tell you where every cent went and exactly why. But I want to be precise about something, because it’s the entire point of this letter: being good with money and being able to enjoy it are two completely different skills.

The early years I was a mess. I fumbled through paycheck to paycheck wondering why I was falling behind. Then I got organized, saw where the cash was actually going, and learned to optimize every inch of it. I teach those learnings in Escape The Clock. What I don’t cover is what I didn’t really learn until I retired: how to spend freely on the things that were never about the goal at all. Sure, I knew how to budget for a trip or a big expense, but that’s still controlled spending. I’m talking about spending without worry. The stuff that exists purely for joy. I had trained one muscle for decades, and when the saving was finally done, it was the wrong one for what came next.

It turns out I had plenty of company, and the numbers are stranger than you’d guess. According to Kiplinger, the average 65-year-old couple with real savings spends only about 2.1% of it a year. Single retirees are even more cautious, at just 1.9%. That’s roughly half of what the math says is safe. Meanwhile, Vanguard finds only about 40% of boomers near retirement are on track to keep their lifestyle, with the typical near-retiree facing a $9,000 annual income gap.

So we have people who are afraid of running out, yet who spend half of what they safely could. That isn’t a math problem. It’s a permission and an information problem, and unlike the market, both of those are entirely yours to fix.

Getting good with money and learning to enjoy it are two completely different skills, and almost no one ever teaches the second one.

It Was Never a Math Problem

Let’s start with the rule almost everyone has heard of: the “4% rule.” Take 4% of your savings in the first year, adjust it for inflation each year after, and the research says your money should last a 30-year retirement. The number came from testing that rate against the worst markets in modern history, to find a level that would have survived even those. It’s a rough guide, not gospel, but it’s the anchor most people know.

Now look again at what retirees actually do: 2.1% for couples, 1.9% for singles. They’re taking half of what the most-quoted rule in retirement considers safe. That gap, the space between what you could spend and what you let yourself spend, is the most expensive thing in retirement, and it’s paid for entirely in unlived life.

I’m no stranger to that. My first year of retirement I withdrew 0%, partly out of worry and partly because I’d prepared well. My second year, I withdrew 5%, not because I needed to, but because it was a good money move. Now, each year, I continue to withdraw whatever makes sense, leveraging the best of the situation in front of me. I moved past the emotional fear and worry, and now focus on what’s logical.

The fear breaks people quietly. One in four retirees from the last decade told Charles Schwab they weren’t financially prepared for the move from building wealth to living on it, not because the money wasn’t there, but because the switch itself blindsided them. I talked it through with Connor Tyson, a chartered financial consultant who has walked thousands of people right up to this moment, and he put it the way I’ve come to believe it: this is psychology, not arithmetic.

The industry doesn’t help, dressing simple choices up in jargon built to make you feel you need an expert’s blessing to touch your own money. You don’t. You just need a system clean enough that you actually trust it. Because a plan you don’t trust is a plan you won’t follow.

The gap between what you could safely spend and what fear lets you spend is the most expensive thing in retirement.

Build a Paycheck, Not a Pile

There’s a big way to reframe your mindset to remove that fear, and it’s my favorite idea in all of this.

A lump sum is terrifying to spend. A million dollars looks like a finite pile under constant attack, and every withdrawal feels like a wound you’re inflicting on yourself.

So instead of staring at a pile you’re afraid to touch, build a paycheck instead.

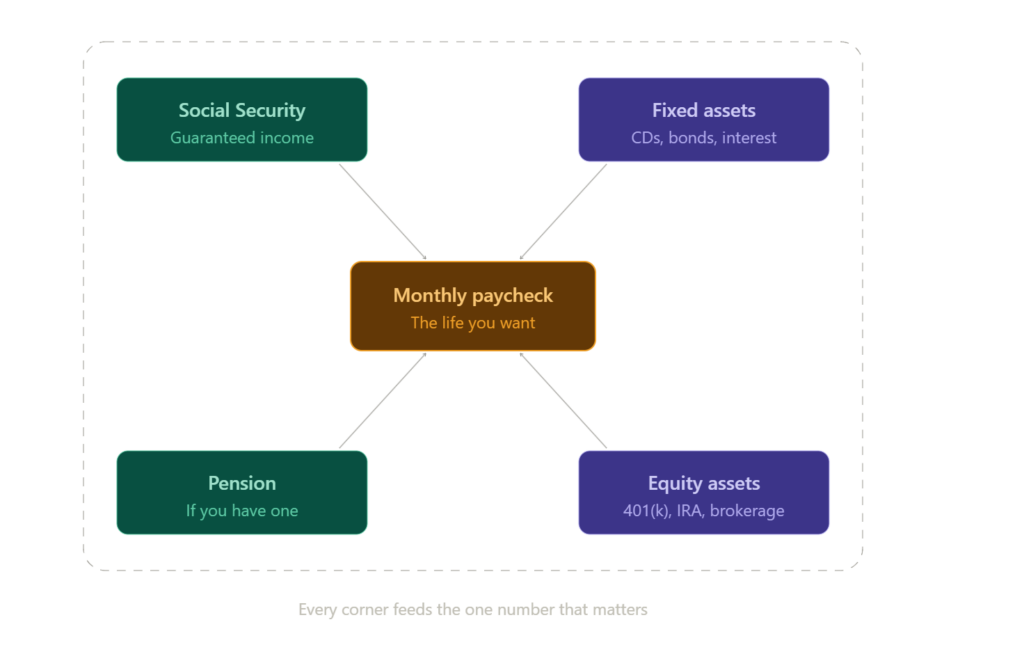

Connor teaches this with a napkin. Draw a square and put one income source in each corner. Top left: Social Security. Bottom left: a pension, if you’re one of the shrinking few who has one. Top right: fixed assets like CDs and bonds, which pay steady interest. Bottom right: equity assets like your 401(k), your IRA, and your brokerage. Then, in the very middle of the square, write the only number that actually matters: the monthly paycheck you need to live the life you want.

Those four corners aren’t equal, and that’s the real lesson of the napkin. The left side, Social Security and a pension, is guaranteed income that shows up no matter what the market does. The right side runs from steady to unpredictable: fixed assets pay reliable interest, while equity assets grow over time but rise and fall with the market. The move is to cover your essential bills with the guaranteed money on the left, then fund everything above that from the right. When your needs rest on a floor that can’t fall, the money that does move stops feeling like a threat.

Now fill it in. Say you want to live on $120,000 a year, round numbers to keep the concept clean, so $10,000 a month. Social Security for a married couple might cover $4,000 of that. No pension, so that corner is a zero. Your fixed assets kick off some interest. Whatever is still missing, you draw from the equity corner.

Doing this flips the script from: “How much of my life savings am I allowed to destroy this year?” to… “Where does this month’s paycheck come from?”

Same dollars. Completely different nervous system.

A paycheck is something you receive, while a pile is something you deplete. You will spend the first one without flinching and guard the second one with your life, even when they are the exact same money. The whole trick of a comfortable retirement is moving yourself, psychologically, out of the second relationship and into the first.

A pile of money is something you deplete. A paycheck is something you receive. Turn the pile into a paycheck, and fear loses its first foothold.

Guardrails: Permission With a Safety Net

If the 4% rule is the floor most people cling to out of caution, guardrails are how you give yourself a raise without losing sleep. A guardrail strategy, sometimes called a dynamic withdrawal strategy, sets a target withdrawal rate and then draws two lines around it: an upper guardrail and a lower one. Say you start by drawing 5% a year, with a ceiling at 6% and a floor at 4%. As long as your spending stays between those lines, you don’t touch a thing. You spend, you live, you don’t agonize.

The lines only matter at the extremes. If a long downturn pushes your withdrawal rate up past the upper guardrail, you trim your spending modestly, often by around 10%, until you’re back inside the lines. And just as importantly, it works the other way. When a strong market pushes your rate below the lower guardrail, the strategy tells you to give yourself a raise. That second half is the part fear-frozen retirees never act on. They’ll take the cut in a bad year on instinct, but they never claim the raise in the good ones, so they spend their entire retirement bracing for a storm that, on average, never comes.

The reason this works is that it replaces a feeling with a rule. You’re no longer asking yourself every month whether you’re spending too much. The guardrails have already answered that, and they’ll tell you the exact day something needs to change.

Connor also has a strategy he calls the reload. Spend down half your portfolio in your early, active years, and let the other half keep working. At a long-term stock return, money roughly doubles every decade, a pace you can estimate with the rule of 72: divide 72 by your expected return, and you get the rough number of years it takes to double. At 7%, that’s a little over ten years. So by the time you’ve worked through the first half of your money, the second half has quietly refilled the tank. The fear says you’re running out. The math says you’re reloading.

Frozen retirees take the pay cut in bad years on instinct, but never claim the raise in the good ones.

Mitigate Fear of Spending with a Liquidity Buffer

There’s one more thing standing between you and spending with confidence, and it’s the fear underneath all the others: bad timing. The nightmare isn’t running out in thirty years. It’s being forced to sell your investments at the bottom of a crash just to cover the grocery bill.

That’s sequence-of-returns risk, and it has wrecked more retirements than bad investments ever have.

The cruelty is in the timing. A steep drop in your first few years, while you’re also pulling out income, shrinks your base so far that even a strong recovery can’t catch up. The exact same drop twenty years in barely leaves a mark.

The fix is almost boring, which is exactly why it works. Keep a cash buffer.

The average bear market runs somewhere between 9 and 14 months. Hold close to a year of living expenses in plain cash, and a falling market stops being an emergency that forces your hand and becomes a storm you simply wait out. You spend from cash, you leave your investments alone to recover, and you return to your normal paycheck once the market does.

And the buffer earns its keep long before retirement. It’s the same wall that protects you from a surprise layoff in an industry doing mass cuts, a medical bill that arrives without warning, or the slow grind of an unexpected expense. It can even be opportunity money, the cash on hand to move fast when something worth buying appears. A buffer is how you make sure the worst day of your financial life is an inconvenience you manage, not a crisis that manages you.

People with cash have options. People without it have ultimatums.

Permission Is the Whole Game

None of these tools works if you won’t give yourself permission to use them. And permission, it turns out, is a practice, not a one-time decision.

The retirees who get this right share three plain habits, and not one of them is about beating the market.

They are:

- Proactive — They plan the money before the month starts.

- Intentional — They tell their money where to go instead of asking where it went.

- Aware — They actually look, auditing the subscriptions and the insurance and the spending at least once a year.

Connor told me he runs his household like a stand-up meeting. You don’t have to go that far, but the principle holds: money is a good servant and a terrible master, and the only way to stay the master is to pay attention on purpose.

Do that, and the fear finally loosens its grip, because you can see exactly what you have and exactly what it’s for. And here’s the thing I had to learn the hard way after a lifetime of being so good at the disciplined half: money is so much more versatile than a means to an end.

We don’t sacrifice for decades so we can die with the biggest balance. We do it so we can stop trading our hours for dollars and start trading our dollars back for hours: for the trip, for the time with the people we love, for the things that were always meant for joy and never for the spreadsheet. That is the entire reason to escape the clock.

Building the freedom is the half everyone obsesses over. Spending it on a life you actually love is the half that was the point all along.

We don’t save for decades to die with the biggest balance. We save so we can trade the dollars back for hours.

Learn More

This issue draws on a recent conversation on Escape The Clock with Connor Tyson, a chartered financial consultant who has helped thousands of people engineer a retirement paycheck and, just as importantly, give themselves permission to spend it.

If this hit close to home, listen to Permission to Spend with Connor Tyson, available wherever you listen to Escape The Clock.

Then go do the work. Map your four income sources and find the one monthly number that actually matters. Set guardrails so you know exactly when, and only when, to adjust. Build a cash buffer big enough to outlast a bad market, a layoff, or a bad year. And then give yourself the one thing no spreadsheet can hand you: permission.

You already did the hard part. You built it. The bravest, and most important, thing left to do is to actually live on it. Go enjoy it and escape the clock!

About the Author

Daniel C. Rodgers is the author of Escape The Clock, the 2025 Best Retirement Book Winner and host of the award-winning Escape The Clock podcast.

“I wasn’t educated for this. I had no financial advantage. Quite the opposite, actually. I started with over $100k of debt and didn’t even know what a retirement account was. Yet, thanks to my career as a Program Manager, I learned the tools I needed to get organized and make that dream a reality.”

If you think this approach could work for you or you’re curious about other options, feel free to schedule a time to connect with me at www.escapetheclock.com. I’d be glad to help you explore the best path for your unique situation.