The Debt Paradox:

When to Burn the Mortgage and When to Leverage It

Escape The Clock Insights

In the personal finance world, there are two distinct religions when it comes to debt: Total Abstinence or Maximum Leverage.

The first church preaches Total Abstinence: Debt is risk. Debt is slavery. Live on rice and beans, cut up the credit cards, and pay off the mortgage as fast as humanly possible.

The second church preaches Maximum Leverage: Debt is a tool. Debt is tax-free money. Borrow cheap, buy assets, and use the bank’s money to scale your net worth faster than your savings ever could.

So, who is right?

If you look at the Federal Reserve’s data, business owners have a median net worth nearly nine times higher than wage earners ($1.3M vs $155k). They didn’t get there by skipping lattes. They got there by using leverage.

However, 25% of Americans say debt is the primary reason they will never retire. They aren’t leveraging; they are drowning.

This week, I spoke with two experts from opposite ends of the spectrum to solve this paradox. Walt Postlewait, a commercial lender who has deployed over $600 million in funding, and Andy Bennetts, a financial educator who uses algorithmic math to eliminate debt in record time.

Together, they reveal the truth: Debt is like a chainsaw. In the hands of a craftsman, it builds a cabin. In the hands of a consumer, it cuts off a leg.

Consumer debt destroys wealth, but strategic debt builds it.

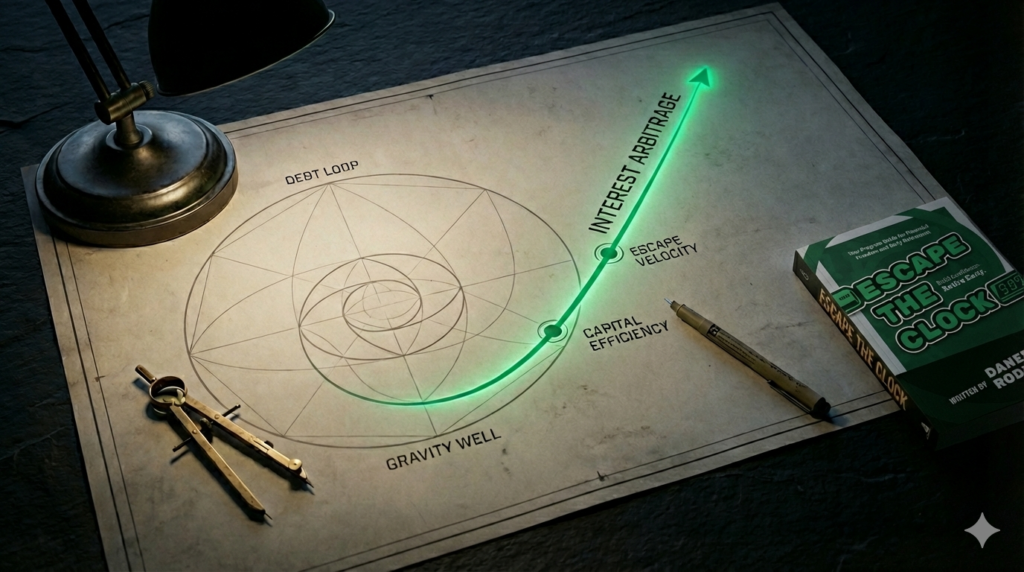

The Generational Debt Loop

Most of us are trapped in what experts call the “Generational Debt Loop.” We are taught to treat monthly payments as static facts of life. We buy a house, sign the 30-year mortgage, and assume that if we make the payment on time, we are winning.

But we are ignoring the Total Interest Percentage (TIP).

We are trained to look at the APR (e.g., 6%). But amortization schedules are front-loaded. On a standard $400,000 loan at 6% over 30 years, the total interest paid is roughly $430,000.

You are effectively buying the house for yourself once, and then buying a second house for the bank. This isn’t an accident; it is a mathematical inefficiency designed to keep you tethered to the system.

Worse, this cycle is hereditary. By going through the motions, we implicitly teach our children to follow the same script. We hand them a roadmap that leads directly to a cliff and they pass it on to their children.

You can’t tame what you cannot name. Blindly following the borrower’s script creates a loop of debt that flows down generations.

The Shift to Strategic Leverage

To escape this loop, we have to stop acting like consumers and start thinking like capitalists.

Walt Postlewait spent 20 years sitting on the other side of the desk, deciding who gets the money and who gets the rejection letter. He explains that wealthy borrowers don’t borrow for things; they borrow for cash flow.

If you borrow at 7% to buy a boat that depreciates, you are destroying your future. If you borrow at 7% to buy a business or a laundromat that returns 25% on cash flow, you are accelerating your freedom.

The goal isn’t to be debt-free forever; the goal is to eliminate consumer debt (liabilities) so you have the capacity to take on strategic debt (assets).

If the debt is related to a depreciating asset… that’s the bad kind of debt.

The Mathematical Exit

So how do we bridge the gap? How do we get from drowning in mortgage interest to buying cash-flowing assets?

There is the Snowball Strategy, where you pay down the lowest balances first to build psychological momentum. And there is the Avalanche Strategy, where you focus on the biggest, scariest debt with the highest interest rate.

But if you really want to kill debt as quickly as possible, you need to use Interest Arbitrage.

Imagine fighting fire with fire. You are borrowing money at a lower rate to pay off higher-rate loans. In essence, you are moving debt, but by doing it this way you are shaving off interest, allowing you to pay less premium. This isn’t any different than refinancing a mortgage, and it can be used to eliminate existing debt and strengthen terms on leveraged loans

Andy’s “Financial GPS” model does all this. He devised a way to make to do the math so that people didn’t have to. It relies on a simple principle: Banks never let money sit idle. Neither should you.

Consider this: if you have savings sitting in a standard account earning 0.1% while you have a mortgage charging you 7% (amortized), you are losing. By utilizing High-Yield Savings Accounts (HYSA) or offset strategies, you can use your cash flow to “cancel out” the bank’s interest curve without actually spending the money until the last second.

It isn’t magic. It is just math. By auditing the flow of your money minute-by-minute, you can shave decades off a mortgage without earning a single extra dollar of income.

APR doesn’t matter as much as the timing and amount in which you pay.

The Cost of Auto-Pilot

How many people in your life borrow money? Is the credit card swipe the default? How about borrowing for leverage? I’m not talking about a car or a house; I mean borrowing as a means to get ahead financially.

The truth is that we live in a system where the norm is consumer debt. Yet, the rich avoid that and instead live off leverage. Sticking with the norm is a sure way to stay poor. But what if you flipped the script? What if you paid off the bad debt and only borrowed toward your financial independence?

It may not be easy, and there will be setbacks. But with a plan, those setbacks are only setbacks, they aren’t catastrophic failures.

Act like a Program Manager. Build a debt elimination project into your plan. Use leverage to speed up your goals. Look at your mortgage and understand how amortization is stacked against you, then make a project plan to take control of that asset. Your program is where you break it all down into easy steps. You’ll get there, one task at a time.

Falling down flat on your face is still forward movement.

Learn More

Whether you are trying to kill a mortgage in 7 years or leverage your first business acquisition, the rules are the same: Respect the math, build the relationships, and never borrow without a plan.

I have two incredible conversations for you to help you build your plan:

- Eliminate the bad debt: Listen to my conversation with Andy Bennetts on The Financial GPS.

- Build leverage with good debt: Listen to my conversation with Walt Postlewait on Borrowing With Intention.

The cost of not doing this is delayed or cancelled retirements, unrealized dreams, and generational poverty. But just because the system profits from our ignorance doesn’t mean we can’t help each other break free.

So share this, or at least sit down and talk about it with the people you care about. We can break the debt cycle one person at a time.

Stop funding the bank’s future and start securing your own. Take control of the debt and escape the clock.

About the Author

Daniel C. Rodgers is the author of Escape The Clock, the 2025 Best Retirement Book Winner and host of the Escape The Clock podcast.

“I wasn’t educated for this. I had no financial advantage. Quite the opposite, actually. I started with over $100k of debt and didn’t even know what a retirement account was. Yet, thanks to my career as a Program Manager, I learned the tools I needed to get organized and make that dream a reality.”

If you think this approach could work for you or you’re curious about other options, feel free to schedule a time to connect with me at www.escapetheclock.com. I’d be glad to help you explore the best path for your unique situation.